Our popular business beat basics series is now available all in one place in ebook form for your convenience. Go here to download the Reynolds Center’s free ebook, Business Beat Basics.

***

Reporters most often use proxies to report on executive pay. This is where proxies shine, thanks to federal rules requiring uniform calculations and disclosure.

The centerpiece of executive pay disclosure is the Summary Compensation Table, typically toward the middle of the proxy statement. It shows up to three years of pay data (the most recent and two prior years) for each of the named officers, providing dollar figures for eight standard categories.

Not chicken feed: Excerpt from the summary compensation table in poultry giant Tyson Foods Inc.’s Dec. 21, 2012 proxy statement.

Note that pay is reported for the year in which it’s earned, so a bonus for performance in 2012 shows up in the 2012 line, even if it was actually paid out early the following year. By contrast, the amounts are calculated as of the time of the award; the value of stock-based pay can fluctuate after that point, for example, but the proxy table effectively offers a snapshot in time.

Salary is just that — cash paid regularly during the year, not directly linked to individual or company performance measures.

Bonus can mean many things, but here it refers to only so-called “discretionary” bonuses: one-time payouts not tied explicitly to a company or individual performance plan. (Incentive bonuses appear three columns later.) The bonus column can include hiring, or “sign-on”, bonuses; special awards; severance; and any number of other payouts. These are usually cash payments, and can often be deferred (see below). Check the table’s footnotes for specifics.

Equity or stock-based compensation appears in the next two columns. Unlike salary, these are essentially estimates: The true value will fluctuate over time with the company’s stock price or other factors. The amounts reported in the table, however, are calculated by more or less uniform methods, as of the date that the awards are made to the executive.

- Stock Awards include ordinary shares of company stock, but more commonly restricted stock or restricted stock units, as well as any performance shares, phantom stock or a variety of other similar instruments. They’re all alike in that the value shown in the table is essentially the stock price multiplied by the number of shares or units the executive gets. The ultimate value will fluctuate with the company’s stock price, but that isn’t reflected here.

- Option Awards includes stock options, but also less familiar instruments like stock-appreciation rights. These are all similar in that the ultimate value to the executive depends on the difference between the share price when he or she receives the awards, and the share price when he or she cashes them in (often years later). The dollar figure shown in the table reflects an estimate or projection, generally calculated with complex but widely used option-valuation formulas.

Non-Equity Incentive Plan Compensation includes a variety of cash payouts tied to the company’s or individual’s performance. The most common is the annual incentive bonus, but many companies also have long-term incentive plans based on two or three years of company performance.

Change in Pension Value and Nonqualified Deferred Compensation Earnings adds together two largely unintuitive amounts. One is the growth of the executive’s pension during the year (not its total value); the other includes some but not all of the interest earned on the executive’s deferred compensation account. The breakdown is usually in a footnote. Some companies try to argue that these amounts shouldn’t be counted as part of a given year’s pay. But it’s compensation for work performed, and amounts the executive will get in the future, in the same way that money put into your 401(k) or pension plan is part of your pay. At the very least, it reflects a growing and sometimes enormous IOU from the company to the executive. There’s more on pensions and deferred compensation in the.

All Other Compensation is just that: a catch-all for special benefits and perks — from souped-up life insurance and discounted sports tickets to free jet rides or even company-subsidized home renovations. Anything over $10,000 must be itemized, usually in a footnote following the Summary Compensation Table or in a separate table (which often has footnotes of its own!). Always look closely.

Even footnotes have footnotes: Part of the footnote for the All Other Compensation column in Tyson Foods’ Summary Compensation Table.

… [several table rows omitted] …

Total is the most valuable column for reporters on deadline. It’s the sum of the other columns, just like it sounds. Some news organizations have formulas to calculate their own version of “total” pay, and companies often argue that other measures make more sense. But this is the universal standard; it’s defined by federal regulation, and comparable across companies. You’re on firm ground if you use it, especially if you tell your audience what number you’re using (“total pay as reported to federal securities regulators,” for example).

You may have noticed several references to footnotes. Read them — they often hold the most interesting and eye-opening details in the proxy.

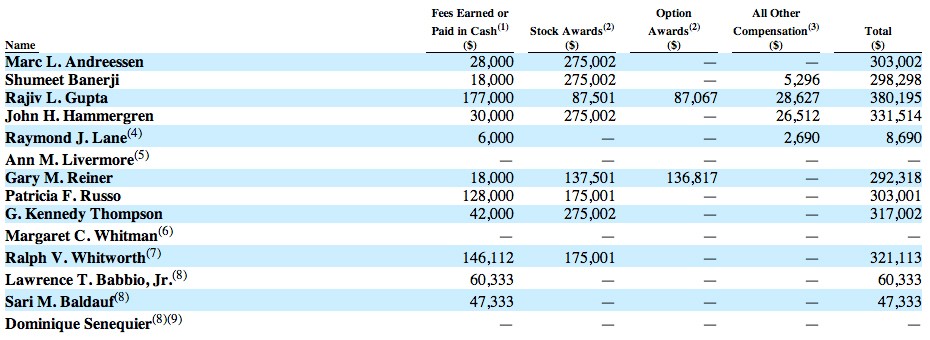

Director compensation is treated much the same way as executive pay, though in a less detailed table covering only the most recent year. Columns vary based on pay practices, but can include fees paid in cash; stock awards; option awards; non-equity incentive awards; pension and deferred-comp gains (which are unusual for directors); and all other compensation, including perks (check those footnotes!), as well as a Total column. Note that this table generally includes only non-employee directors — executives who also sit on the board are usually in the Summary Compensation Table, not here.

Part-time work: The director compensation table from the preliminary proxy Hewlett Packard Co. filed on Jan. 11, 2013.

The most extensive compensation section in the proxy tends to be the least useful: the Compensation Discussion and Analysis, or CD&A (sometimes mis-heard as “CDNA”). This is usually long on boilerplate and justification, and short on useful detail. Still, companies are supposed to explain how executives got what they did, and why. Don’t ignore it — sometimes the reasoning for lavish perks can be amusing, and the contrast between what a company says and does can be newsworthy. Tables in this section also provide numbers that can be useful, such as bonus targets for the following year. Just understand that it can be a morass to decipher.

There’s plenty of other information on compensation throughout the proxy.