Our popular business beat basics series is now available all in one place in ebook form for your convenience. Go here to download the Reynolds Center’s free ebook, Business Beat Basics.

***

A newly issued proxy can generate news on its own — when a CEO’s pay doubles, lavish perks contrast sharply with layoffs and cost-cutting, or a shareholder wages a proxy fight, for example. But it’s also a useful reference tool for stories that originate with other events or ideas.

We’ll walk through some different ways a proxy can be useful, both as a primary news element, and in supporting roles.

ALL IN A YEAR’S WORK

1. Pin the raise (or the pay cut) on the CEO

This is a tried and true approach: Use the Summary Compensation Table to calculate the increase or decrease in the total pay of the chairman or CEO. If the CEO is newly appointed, you can usually compare his pay to his predecessor’s, though you may need to pull the prior year’s proxy to do so. For long-time CEOs, consider looking at multi-year trends.

2. Take stock (and options, and cash…)

Don’t forget to compare how different components of pay have changed. More cash and less stock could indicate managers have little incentive to generate good returns for shareholders. More stock and less cash means more of an executive’s pay is at risk — which could spur better management, or a riskier swing-for-the-fences mentality; it may also suggest management and the board are bullish about the future. Weigh the possibilities by talking to compensation experts and investors and analysts knowledgable about the company.

3. Unscramble the nest-egg

MORE on PROXY

STATEMENTS

An introduction

Tips for using the proxy

Traps and mistakes

Compensation basics

Glossary of key terms

Resources

Be sure to check the sixth column, showing pension and deferred-comp changes. As executives approach retirement age, pension values can skyrocket. A dedicated pension-benefits table, which usually follows the summary-comp table, gives more detail. It lays out not only the annual increase, but also a total “present value” of the pension — its value in today’s dollars, a number that can be enormous. Footnotes or text nearby explain underlying pension formulas and other context, though often the numbers are enough. For example, McKesson Corp.’s 2011 proxy showed that Chairman and CEO John Hammergren’s pension at $83.4 million; the following year, it had risen to $92.6 million — gaining 11% in one year (and nearly doubling over three years).

If the footnotes for the sixth column show big bucks from an executive’s deferred-compensation account, check the deferred-compensation table, which usually follows the pension section. It breaks down how much each executive set aside in deferred pay the prior year — roughly the equivalent of a super-charged 401(k) plan (See the Glossary) — as well as how much the company contributed to the account during the year, which can be significant. Other columns show gains or losses on the account (which the company pays) and any amounts the executive withdrew during the year. The total column gives the executive’s account balance as of the end of the last fiscal year.

Golden years: The pension-benefits table is typical; the pensions’ size isn’t.

A penny saved adds up to $26 million earned for Hammergren. Sometimes you have to add up multiple rows to get an executive’s total.

4. Perk things up a bit

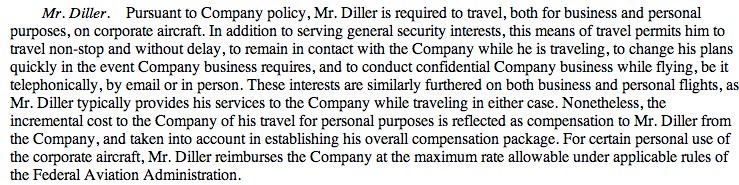

Perks and special executive benefits make great articles and attract attention. The details are usually in a footnote to the Other Compensation column of the Summary Compensation Table, or a nearby table of their own. In the Compensation Discussion and Analysis section, the company often justifies the various perks briefly. In a typical disclosure, for example, IAC/InterActiveCorp says it pays for Chairman Barry Diller’s personal trips on company jets, arguing it’s safer for Diller and more convenient for the company.

Friendly skies: IAC/InterActiveCorp requires its chairman to use the private jet for “general security” and the company’s convenience.

LOOKING BEYOND PAY

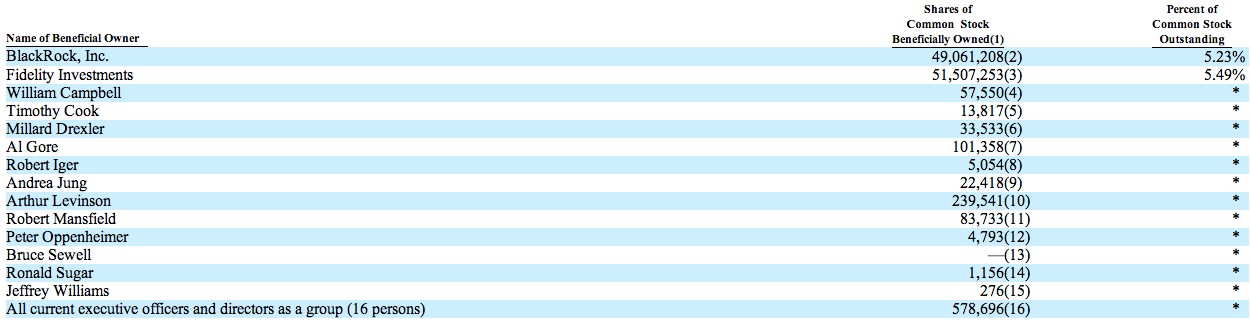

5. Stake out the owners

A table of beneficial owners shows how many shares of company stock are held by each director and named executive, plus an aggregate number for all directors and officers. It also shows the stakes of major shareholders (those owning 5 percent of shares or more). This is a snapshot in time, as of the end of the last fiscal year.

Look here during takeover battles, to see how much say management has on its own. You can also use it to quantify how much an executive has lost or gained (on paper) from sudden changes in share price. Or if there’s a merger under way, or the company is being acquired or taken private, you can estimate how much executives will make on their shares. Just multiple the share count listed here by the change in stock price, or for deals, the proposed share price for the sale.

Big names: The beneficial owners table from the definitive proxy filed by Apple Inc. on Jan. 7, 2013.

6. Untangle ties that bind

Corporate directors and the executives they supervise sometimes have business dealings or other relationships going well beyond the company they run together. Those ties are supposed to be laid out in the related-party transaction disclosure (sometimes labeled “related persons,” “related transactions” or other terms). Relationships can be direct or through other entities, such as a director’s employer or an executive’s family trust or investment partnership.

Some real-life examples from years past: A company that rented the chairman’s fishing lodge for business entertainment, another that paid millions for the CEO’s map collection, companies that lease jets owned by the CEO for business trips (and at least one that also paid for the executive’s personal trips in his own plane), and directors whose law firms do six-figure business with the company.

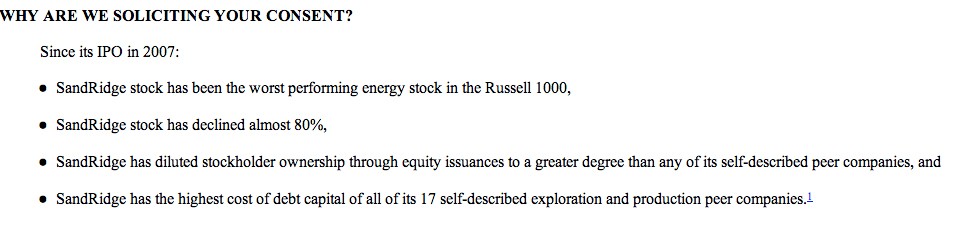

7. Emcee a proxy fight

Proxy fights don’t come around often, but they’re news when they do. Typically, a big investor puts forward one or more candidates to contest incumbent directors, who generally run unopposed. For now, activist investor must produce and distribute proxy materials themselves, making the case against the company’s existing management; it’s an expensive proposition. Moreover, proxy fights often come after months of behind-the-scenes negotiations with the sitting board, so shareholders that go this far are usually pretty serious.

These are typically straightforward conflict pieces, but don’t forget to mine the documents for key details mentioned above, including sizing up the stakes each side has in the company, and looking for potential conflicts in the related-party disclosures and director bios.

Then keep up with the filings, since both sides may file rebuttals until shortly before the annual meeting.

Not subtle: Excerpt from a Jan. 15, 2013, proxy solicitation (DEFC14A filing) to shareholders of Sandridge Energy by private-equity firm TPG Capital, which is seeking to oust the company’s board.

8. Tallying votes that count (sort of)

Don’t forget the items facing a vote: shareholder and management proposals. These often appear near the end of the filing. Some are routine — renewing the outside auditing firm’s contract, for example. But even there, pay attention when companies switch to smaller, lesser-known auditing firms: It can be a sign of trouble.

The more interesting proxy measures tend to be proposed by unhappy shareholders. Some are essentially political or social statements: Tyson Foods is routinely asked to treat its chickens more humanely, while Apple in 2012 faced an unusual demand to elaborate on directors’ potential conflicts of interest, from a D.C. think-tank that suggested Al Gore had benefited financially from company policies (an allegation Apple rejected). Other proxy measures turn on broader philosophies of corporate governance, such as separating a company’s chairman and CEO positions, or giving big shareholders a more direct say in calling special meetings. | Video: A Walk-Through of Apple’s Proxy with Theo Francis

Companies provide detailed rebuttals to proposals they oppose (which is most of them). Some of these shareholder proposals appear dry, but can actually reflect a bid by unions or an activist investor to make it easier later on to challenge management or put outside faces on the board. Such challenges generally aren’t subtle, so read the arguments on both sides to figure out what’s going on.

In the end, these shareholder proposals tend to be advisory proposals, meaning the board can ultimately ignore them — but there are often longer-term consequences for antagonizing shareholders, such as a proxy battle with dissatisfied hedge funds.

9. Watch for changes

If you spot a preliminary proxy statement (PRE 14A filing) before the final version comes out, use it to write about the company as you would with the real thing; just tell your audience that it’s preliminary. You can get a jump on the competition that way. Just realize some information may be missing — and be sure to check for changes when the definitive proxy comes out. (An easy way to do that: Load both documents into Microsoft Word and use its “compare documents” feature.)